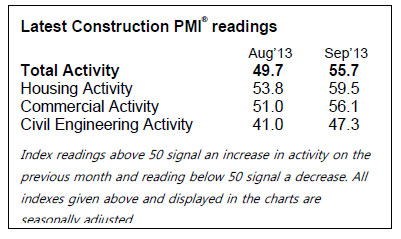

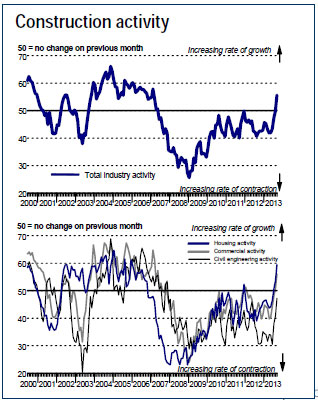

The Irish construction sector returned to growth in September as activity rose for the first time in more than six years. New orders expanded at a sharp and accelerated pace, leading to growth of purchasing activity and a stabilisation of employment. Meanwhile, sentiment among construction firms regarding the 12-month outlook was one of the strongest in the history of the series. The Ulster Bank Construction Purchasing Managers’ Index® (PMI®) – a seasonally adjusted index designed to track changes in total construction activity – posted 55.7 in September, rising from 49.7 in August and registering above the 50.0 no-change mark for the first time since May 2007. Panellists reported that higher new orders and signs of improvements in economic conditions had contributed to growth of activity.

Commenting on the survey, Simon Barry, Chief Economist Republic of Ireland at Ulster Bank, noted that:

“The September results of the Ulster Bank Construction PMI provide further evidence of improved trends in the Irish construction sector. Significantly, overall activity rose for the first time in over six years, as the headline PMI index jumped by 6 points to get back to above the 50 breakeven level for the first time since May 2007. Housing was again the strongest sub-sector, as activity expanded at its fastest pace since December 2005 following a third consecutive above-50 reading. Commercial activity also saw an acceleration in its rate of expansion last month, and while respondents continue to report falls in Civil Engineering activity, the pace of decline eased to its slowest in some six years.

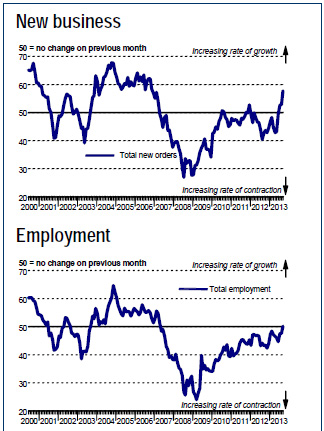

“The September results show that the nascent recovery in activity levels is producing a stabilisation of employment among survey respondents. The employment index rose to just over the 50 mark last month, breaking a sequence of declines in staffing levels that extends back to May 2007. However, firms reported that cost considerations continue to weigh on their hiring plans – an indication that respondents remain understandably cautious following what has been a brutal downturn for the sector. Nevertheless, forward-looking elements of the survey offer encouragement about future prospects. New orders recorded a third consecutive monthly rise as firms reported rising new business levels at home and overseas, while there was also a further improvement in business sentiment, with optimism about the 12-month outlook reaching the strongest since January 2004.”

Sharp expansion in residential activity

The sharpest increase in activity was seen on housing projects in September, with the rate of expansion the steepest since December 2005. Commercial activity also rose at a marked and accelerated pace during the month. Although civil engineering activity continued to decrease, the rate of contraction eased sharply to the slowest in the current 70-month sequence of decline.

New order growth accelerates

Contract wins in both domestic and overseas markets led to a substantial rise in new orders during September. New business increased for the third month in a row, and at the fastest pace since November 2006.

First rise in input buying in over three years

Rising workloads led to an expansion of purchasing activity, the first increase in just over three years. Furthermore, the rate of growth was marked. Construction firms’ use of sub-contractors also rose during September. The availability of sub-contractors fell back slightly, while they increased their rates charged for the first time since October 2009.

Staffing levels stabilise

Employment stabilised at Irish constructors, ending a sequence of job cuts which began in May 2007. Those respondents that raised staffing levels indicated that this was largely reflective of increased workloads.

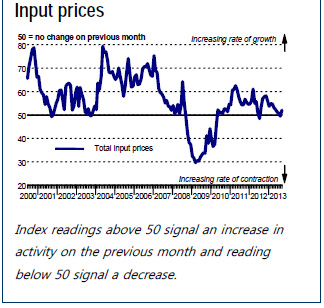

Lead times on the delivery of inputs lengthened again in September, extending the current sequence of deterioration to 27 months. Panellists attributed this to low stock levels at suppliers and raw material shortages. That said, lead times lengthened at the weakest pace in three months. Input prices rose, following a marginal fall in the previous month. However, the rate of cost inflation was only modest and much slower than the long-run series average.

Sentiment strengthens further

Optimism regarding the 12-month outlook for activity picked up to the joint-third highest in the series history in September. Predictions of improvements in economic conditions and more aggressive marketing were forecast to lead to higher new orders and activity over the coming year.

Simon Barry

Chief Economist Republic of Ireland

Ulster Bank

t: 01 6431553

m: 086 3410142

g: 01 6431688

e: simon.barry@ulsterbankcm.com

w: www.ulsterbankcapitalmarkets.com

3rd Floor Dealing Room

Ulster Bank Group Centre

George's Quay, Dublin 2

The Ulster Bank Construction PMI is issued exclusively for the general information of clients, contacts and staff of Ulster Bank. The contents are not a substitute for specific advice and should not be relied upon as such. Accordingly, whilst every care has been taken in the preparation of this publication, no representation or warranty is made or given in respect of its contents and no responsibility is accepted for the consequences of any reliance placed on it by any person.